Wed, Feb 11, 2015

Established industries often beat new technology when it comes to long term returns, while “sin stocks” outperform in the long run, showing that responsible investors do sometimes pay a price for their principles, a new study shows.

The research was revealed in the Credit Suisse Global Investment Returns Yearbook and Credit Suisse Global Investment Returns Sourcebook, which was released today.

In the 2015 Yearbook, the authors, Elroy Dimson, Paul Marsh, and Mike Staunton of the London Business School, examine two issues: first, the long-run rise and fall of industries and the implications for investors; second, the rationale, costs and benefits of responsible investing.

Published by the Credit Suisse Research Institute in collaboration with London Business School, the 2015 Sourcebook reports the latest long-run return data and risk premium estimates for international stock and bond markets, and the performance to the start of 2015 from style factors such as size, value and growth, income, and momentum.

Giles Keating, Head of Research and Deputy Global CIO for Private Banking and Wealth Management at Credit Suisse, said: “The rise of new industries and the importance of responsible investing are two issues that have assumed a lot of importance in recent times. Within that context, it is timely that the 2015 Credit Suisse Global Investment Returns Yearbook examines both the implication and benefits of long-term responsible investing.”

Stefano Natella, Head of Global Securities Research for Investment Banking at Credit Suisse, said: “The Yearbook has a strong track record of identifying important issues for investment strategy across asset classes. It provides valuable guidance for investors by leveraging a proprietary set of long historical data. At a time when investors are confronted by the prevailing volatility in capital markets, the Yearbook provides investors with a unique source with which to make investment decisions.”

2015 YEARBOOK

The Yearbook comprises three articles, together with profiles of 23 national and three regional markets. For each of these countries and regions, it shows the inflation-adjusted returns since 1900 on stocks, bonds, cash and currencies, as well as equity and bond risk premia.

Industries: their rise and fall

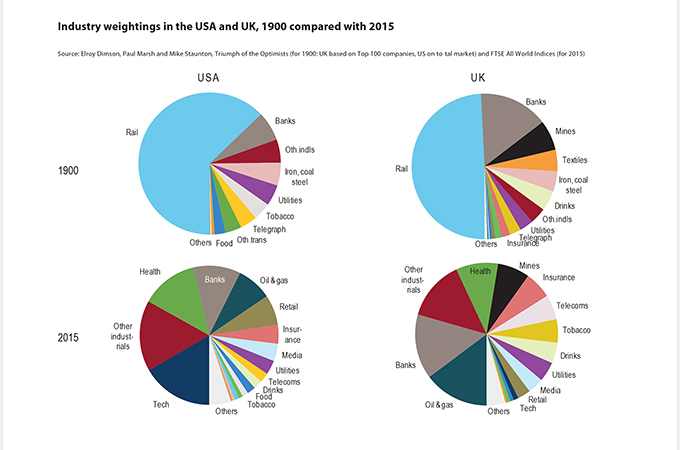

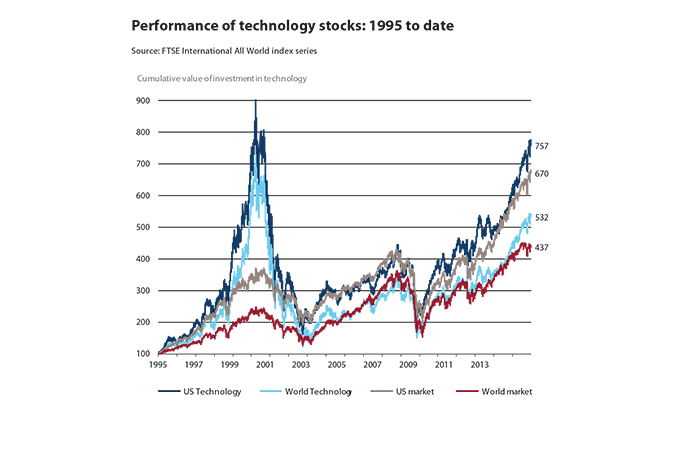

In this article, Elroy Dimson, Paul Marsh and Mike Staunton show that although successive waves of new technology have transformed the world, investors have not always been the main beneficiaries. Stock markets in 1900 were dominated by industries such as railroads which today have small weightings or are extinct. Meanwhile, today’s markets have high weightings in industries that were small or non-existent in 1900, such as information technology, telecommunications, aerospace, oil and gas, pharmaceuticals and biotechnology. Yet the authors show that US railroad shares outperformed the market over the last 115 years, while investment in new technologies has sometimes frustrated investors.

The authors describe how new industries are born on waves of IPOs, which, as a group, have underperformed. Stock returns tend to be higher for seasoned stocks, with older companies outperforming newer ones. They find that industry rotation based on value has generated a premium. This is consistent with there being periods of overvaluation for growth industries which this rotation strategy helps avoid; and periods of undervaluation for value industries which the strategy exploits.

Paul Marsh, Emeritus Professor of Finance, London Business School, notes, however, that: "Momentum appears to be an even more effective industry rotation strategy. Buying last years’ best-performing industries while shorting the 20 per cent of worst performing industries would, since 1900, have given an annualised winner-minus-loser premium of 6.1 per cent in the US and 5.3 per cent in the UK. Before costs, US investors would have grown 870 times richer from buying winning industries rather than losers."

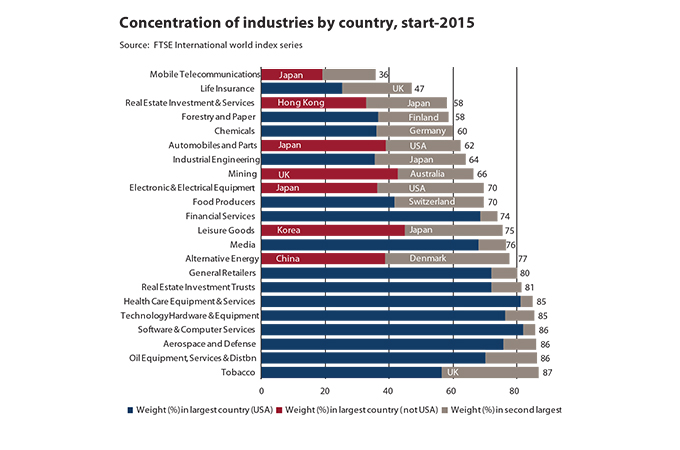

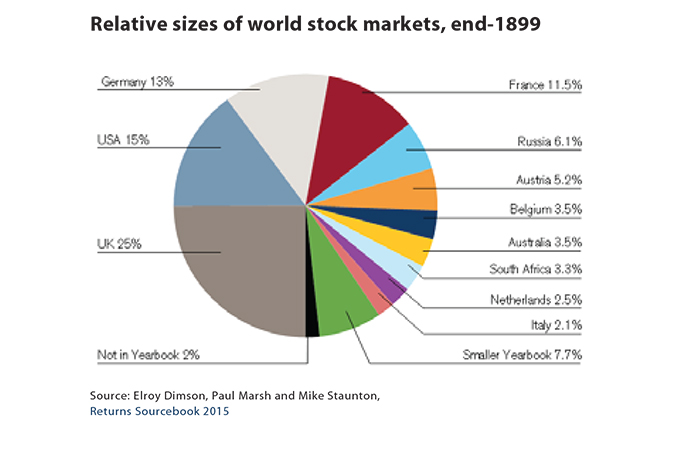

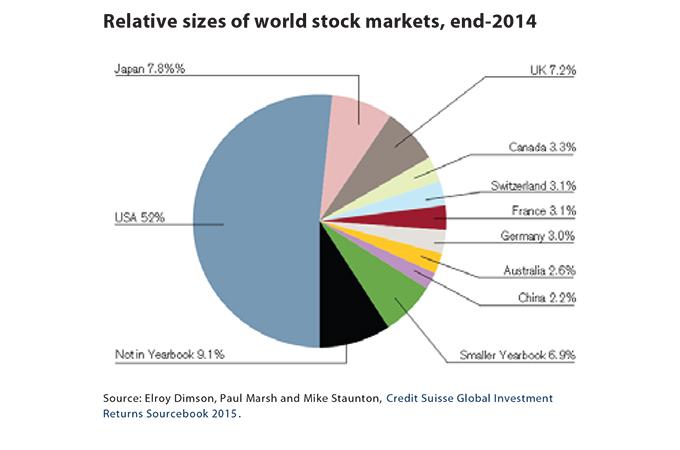

The authors also show that many countries’ stock markets are highly concentrated within a few industries, while many industries are concentrated within a few countries. They conclude that, to exploit diversification opportunities to the full, investors need to diversify across a wide spread of industries and countries. Both matter, although there is evidence that globalisation has led to a decline in the relative importance of countries, with industries assuming greater importance.

Responsible investing: does it pay to be bad?

In the second article, the authors turn to an issue that has recently preoccupied asset owners: how to construct a responsible investment strategy? Investors are increasingly concerned about social, environmental and ethical issues, and asset managers are under pressure to be responsible investors. This can take the form of “exit” via ethical screening, or “voice” through engagement and intervention.

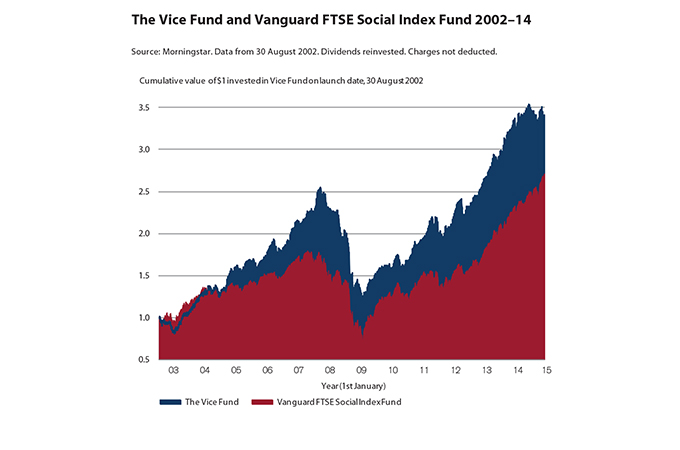

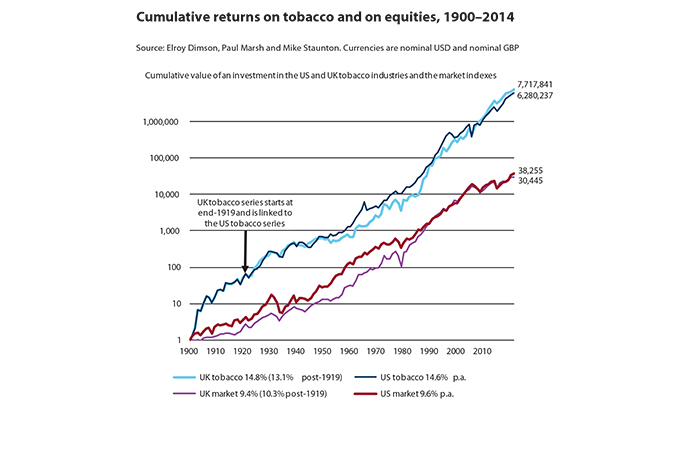

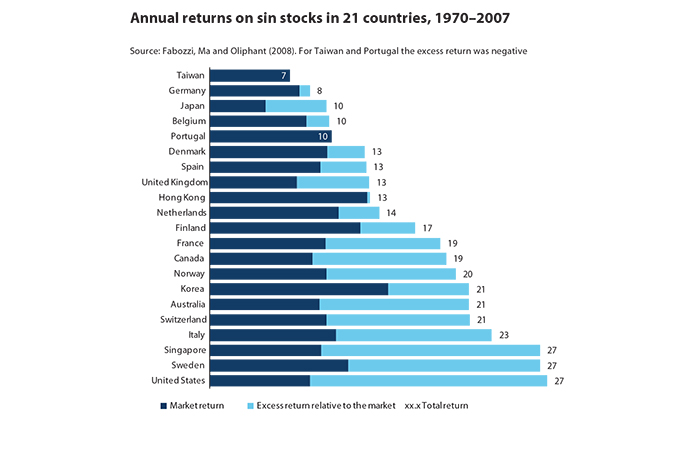

“’Exit’ typically involves excluding companies, industries or countries regarded as distasteful or unethical. However, principles can have a price, since sin stocks may perform well, as illustrated by the strong historical performance of the Vice Fund. Similarly, Dimson, Marsh and Staunton find that the best-performing industries since 1900 have been tobacco in the US and alcohol in the UK. They review other research studies that confirm the superior long-run performance of sin stocks, and during recent years, they find better returns from the most corrupt countries.

Elroy Dimson, Emeritus Professor of Finance, London Business School and Chairman of the Newton Centre for Endowment Asset Management at Cambridge University, suggests that: “Ironically, responsible investors may be partly responsible for the higher returns from sin. If a large enough proportion of investors avoids sin businesses, their share prices will be depressed, thereby offering the prospect of elevated returns to those less troubled by ethical considerations”.

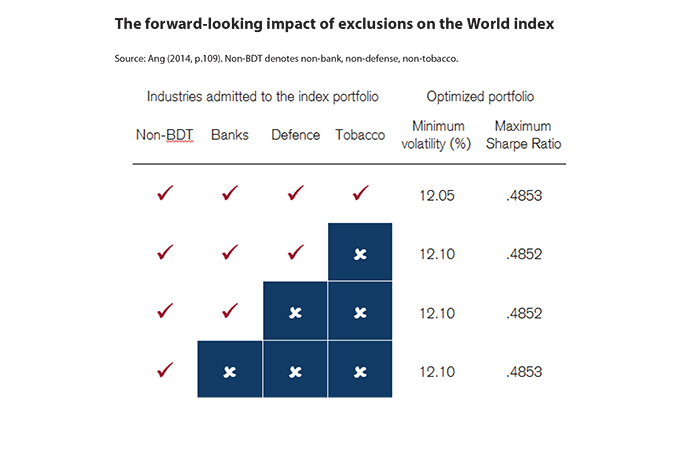

The authors report that the expected financial impact of modest exclusions is generally small. They find that use of “voice” can pay, whether the focus is on environmental and social issues or on corporate governance. Engaging with companies owned by the investor is shown to be profitable in a number of cases, especially when action is co-ordinated with like-minded activists. The authors commend a strategy of rotating investment across a range of businesses. When active owners influence corporate behavior for the better, financial performance also tends to be better.

Do equity discount rates mean revert?

The third article is by David Holland and Bryant Matthews of Credit Suisse HOLT. They examine how the market-implied cost of capital mean reverts over time and the extent to which this is in any way predictable. They find that, at the country level, China and Switzerland currently have the lowest market-implied discount rates, while Russia, Italy and Argentina have the highest.

2015 SOURCEBOOK

Now covering 26 markets, the Sourcebook examines risk over the long run and the historical extremes of investment performance. It documents the global long-term and shorter-term rewards for equity and bond investing, and presents the detailed 115-year dataset that underpins the Credit Suisse Global Investment Returns Yearbook. The authors report that, notwithstanding a strong recovery since 2009, world equity performance has still been disappointing since the start of 2000, especially relative to bonds. However, over the long run, equities have beaten inflation, bonds and cash in every country with a continuous 115-year history.

The Sourcebook also investigates the impact of investment styles on portfolio performance, emphasising size, value, income and momentum effects in stock returns. The authors report a size premium (the amount by which smaller companies outperform larger ones) that has been positive over long intervals and many countries; a value premium (the amount by which value stocks outperform growth stocks) that has been larger than the size premium; an income premium (the amount by which high-yielding stocks outperform low-yielding stocks) that has been larger than the value premium; and a momentum premium (the amount by which past winners outperform past losers) that is largest of all.

Credit Suisse is one of the world's leading financial services providers and is part of the Switzerland’s Credit Suisse group of companies. Credit Suisse is headquartered in Zurich and operates in over 50 countries worldwide.

London Business School’s vision is to have a profound impact on the way the world does business. The school is consistently ranked in the global top 10 for its programmes and research and celebrates its 50th anniversary this year.

The 2015 Yearbook is available as a free download, while the 2015 Sourcebook is a hard-copy publication and can be sent only by post.